Each flow of funds detailed in this guide has unique status workflows that are important to understand to properly track and reconcile payments and manage risk.

Transfer Statuses

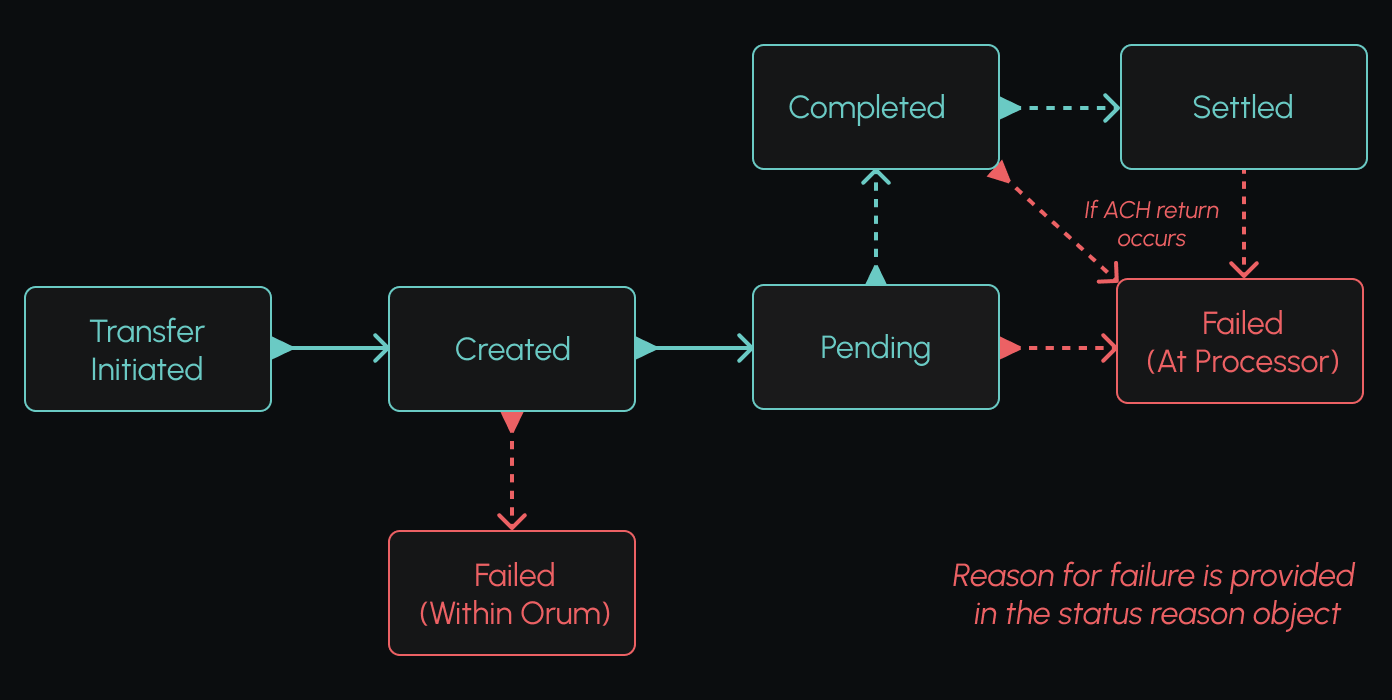

Created

Pending

Completed

Settled

Failed

The request was received and a transfer was created.

The transfer request is processed by Orum and is run through a series of validation checks regarding the use case, balances, and the status of the parties and accounts in the request.

The transfer request has been submitted to the payments network. This does not indicate the successful settlement or delivery of funds. For settlement or expected posting times, use the estimated funds delivery date to know when the funds will land in the destination account or in your Orum balance. A debit transfer has settled, which means the funds have moved from your pending balance to your available balance and are available for use.

A transfer failed. The failure could have occurred either in Orum’s system or at the processor. Refer to the network and reason codes guide for more information. All transfers that fail due to a validation error (e.g. insufficient funds in your Orum balance, not eligible for the attempted flow of funds) before they are processed by a bank will cycle from created —> failed, and will never have a status ofpending.

Flows of Funds

Account-to-Account (A2A)

Account-to-Account transfers, or “dual-leg” transfers, are easily processed by including both a source and destination in the transfer request. Account-to-Account transfers consist of two separate transactions:

- The first transaction is an ACH debit to pull funds from the source into your Orum balance at Orum’s originating bank.

- Once the funds from the first transaction have settled, the second transaction is a credit to push funds to the specified destination. The credit payment rail will be dependent on the instrument of the destination (bank account), the speed parameter chosen in the request, and the receiving accounts rail eligibility.

A2A Flow

You can also do A2A transfers through subledgers by specifying the subledger ID in the A2A transfer request. Funds from the first leg will settle into the subledger and the second leg will pull from the balance of the subledger. Any returns will also be debited or credited to the subledger in the case of a debit or credit failure.

You can also do A2A transfers through subledgers by specifying the subledger ID in the A2A transfer request. Funds from the first leg will settle into the subledger and the second leg will pull from the balance of the subledger. Any returns will also be debited or credited to the subledger in the case of a debit or credit failure.

Subledgers are a great way to keep customers’ funds segregated and are required for any use cases that involve payments being embedded into a platform that is considered a nested third party sender.

A2A Scenarios

It is very important to note that there is risk of returns/chargebacks for both legs of an A2A transfer and each return scenario has implications on how a failure needs to be addressed.

The diagram below shows the transfer status workflow for an Account-to-Account transfer. When there is a transfer failure, the responses will specify if the failure was at the source or destination. The following section will detail the responses you can expect via webhook, what you will see in Monitor, and explain what happens to the funds.

A2A Scenarios

It is very important to note that there is risk of returns/chargebacks for both legs of an A2A transfer and each return scenario has implications on how a failure needs to be addressed.

The diagram below shows the transfer status workflow for an Account-to-Account transfer. When there is a transfer failure, the responses will specify if the failure was at the source or destination. The following section will detail the responses you can expect via webhook, what you will see in Monitor, and explain what happens to the funds.

Transfer Completes With No Failures

In a normal A2A transfer flow when there are no returns on either leg, the transfer request will go from a ‘created’ to ‘pending’ status and remain in that status for the first leg while funds are pulled onto the platform from the source account. The amount of the transfer will be in your pending balance.

Once the hold time on the debit is met and the debit successfully settles into your available balance, the credit leg is submitted for processing and the transfer moves to a ‘completed’ state. This signals that both legs have been processed successfully and the estimated funds delivery date tells you when funds should post in the destination account.

Transfer Completes With No Failures

In a normal A2A transfer flow when there are no returns on either leg, the transfer request will go from a ‘created’ to ‘pending’ status and remain in that status for the first leg while funds are pulled onto the platform from the source account. The amount of the transfer will be in your pending balance.

Once the hold time on the debit is met and the debit successfully settles into your available balance, the credit leg is submitted for processing and the transfer moves to a ‘completed’ state. This signals that both legs have been processed successfully and the estimated funds delivery date tells you when funds should post in the destination account.

Please note that when funds post is ultimately up to the RDFI.

status_reason will specify that the failure occurred on the source account.

A Debit Return will include the reasons for the failure — including Orum reason codes/messages and network codes/messages — so that you know the cause and type of return. This information is also available in Monitor by clicking on a transfer to open the transfer details page.

- Tardy returns that happen outside of Nacha’s two business day return window

- Configuration for accelerated debit hold times of less than two days given that credits are processed before the Receiving Depository Financial Institution (RDFI) is required to send returns back.

- Unauthorized returns like an R10 that can happen days or even weeks later

When you see an A2A transaction change status from ‘completed’ to ‘failed’ and the failure is from the source account, you know that the debit leg returned after the credit has already been processed.

This can cause your balance or a subledger balance to go negative and insufficient funds errors for other transactions.

- Keep a pre-funded balance on the platform to absorb these loss causing transactions so that you always have a sufficient available balance.

- Troubleshoot the cause of the return with your customer and submit a new request to debit their account using a single leg debit. Provide the source details and leave the destination blank. A successful retry will bring your balance back to neutral.

- If you have a negative balance, you can top-up your balance back to zero.

If one of the above methods is not utilized to get back to zero, Orum will eventually transfer funds from your collateral balance and we will ask you to refill your collateral balance.

- Send a new credit transfer to the destination over a different rail or after updating the account details if they were inaccurate

- Send a new credit transfer to the source to return the funds back to the sender.

Orum does not retry credits or send funds back to the source automatically. Orum leaves that up to our customers and you must submit a new single leg transfer.

Payouts

Payouts or credit/push transactions using your Orum available balance are processed by sending a transfer request with only a destination and leaving the source blank or designating a subledger as the source.

Credit transactions require an available enterprise or subledger balance that is equal to our greater than the amount of the transaction(s). If the balance is insufficient you will receive an insufficient funds error.

Below are visual representations of Payouts from an enterprise balance and a subledger balance.

Credit transactions are far simpler than A2A and Debit transfers. As with any payment, credit transactions can return for various reasons. This is usually due to admin ACH returns (R02, R03, R04) or there are times a realtime payment will fail due to the recipient bank (RDFI) not being online due to a network outage or planned maintenance.

Credit transactions are far simpler than A2A and Debit transfers. As with any payment, credit transactions can return for various reasons. This is usually due to admin ACH returns (R02, R03, R04) or there are times a realtime payment will fail due to the recipient bank (RDFI) not being online due to a network outage or planned maintenance.

Reason and Network codes for RTP/FedNow can be found here. Cards have their own network reason codes, which can be found here.

-

Send a credit transfer to the destination over a different rail. This generally means downgrading from a speed of “asap” and using “same_day” or “standard” so that the payment is processed by ACH instead of RTP/FedNow.

Card payments always use a speed of “asap” and failures are generally due to a lack of push functionality or restrictions by the issuing bank.

-

Reach out to the user to confirm account/card details to see if they were inaccurate and send a new credit transfer after updating the information.

The standard status workflow for a credit transfer is detailed in the diagram below.

Deposits

Deposits, or debit/pull transactions used to pull money into your Orum balance, are processed by sending a transfer request with only a source and leaving the destination blank or by specifying a subledger as the destination.

Below are visual representations of Deposits to an enterprise balance and a subledger balance:

Debits do not immediately settle into your available balance. Depending on the payment rail used and your hold time configuration, these funds will remain in your pending balance until hold times are met and funds are settled.

It is very important to note that there is risk of returns/chargebacks with all debit/pull transactions. The following section will detail the responses you can expect via webhook, what you will see in Monitor, and explain what happens to the funds.

Transfer Completes With No Failures

In a normal Debit/Pull transfer flow when there are no returns or chargebacks, the transfer status will go from ‘created’ to ‘pending’ to ‘completed’, signifying that the transaction was successfully submitted to the payment network of the rail being used.

The amount of the transfer will be credited to your pending balance. Once the hold time on the debit is met it will move to a ‘settled’ status and funds will move from the pending to available enterprise or subledger balance.

Debit Return (Source Failure) Before Transfer Completes

If the debit fails due to a return prior to settling, the funds in your pending balance will be removed. The webhook response will update the status of the transfer to ‘failed” and the status_reason will include Orum reason codes/messages and network codes/messages so that you know the cause and type of return. This information is also available in Monitor by clicking on a transfer to open the transfer details page.

Debit Return (Source Failure) After Transfer Settles

ACH debits and Card Pull transactions always hold some level of risk and in some cases, the debit can fail after it has settled. This can happen for a number of reasons and it is important to familiarize yourself with the payment networks’ rules on returns and chargebacks.

A few common failure examples are listed below:

Debits do not immediately settle into your available balance. Depending on the payment rail used and your hold time configuration, these funds will remain in your pending balance until hold times are met and funds are settled.

It is very important to note that there is risk of returns/chargebacks with all debit/pull transactions. The following section will detail the responses you can expect via webhook, what you will see in Monitor, and explain what happens to the funds.

Transfer Completes With No Failures

In a normal Debit/Pull transfer flow when there are no returns or chargebacks, the transfer status will go from ‘created’ to ‘pending’ to ‘completed’, signifying that the transaction was successfully submitted to the payment network of the rail being used.

The amount of the transfer will be credited to your pending balance. Once the hold time on the debit is met it will move to a ‘settled’ status and funds will move from the pending to available enterprise or subledger balance.

Debit Return (Source Failure) Before Transfer Completes

If the debit fails due to a return prior to settling, the funds in your pending balance will be removed. The webhook response will update the status of the transfer to ‘failed” and the status_reason will include Orum reason codes/messages and network codes/messages so that you know the cause and type of return. This information is also available in Monitor by clicking on a transfer to open the transfer details page.

Debit Return (Source Failure) After Transfer Settles

ACH debits and Card Pull transactions always hold some level of risk and in some cases, the debit can fail after it has settled. This can happen for a number of reasons and it is important to familiarize yourself with the payment networks’ rules on returns and chargebacks.

A few common failure examples are listed below:

- Tardy returns that happen outside of Nacha’s two business day return window

- Configuration for accelerated debit hold times of less than two days given that credits are processed before the RDFI is required to send returns back.

- Unauthorized ACH returns like an R10 and card chargebacks due to consumer disputes, both which can happen days and weeks after a transaction is processed.

When you see a debit/pull transaction change status from ‘settled’ to ‘failed’, you know that the debit leg returned after funds were made available to you. If those funds were used for a payout and are no longer in your Orum available balance, this can cause negative enterprise/subledger balances and potentially create a loss causing event. It is important to know what you can do to solve this issue and recoup funds or avoid disruption to your other transaction activity:

- You can keep a pre-funded balance on the platform to absorb these loss causing transactions so that you always have a sufficient available balance.

- You can troubleshoot the cause of the return with your customer and submit a new request to debit their account/card. A successful retry will bring your balance back to neutral.

- If you have a negative balance, you can Top Up your balance back to zero.

If one of the above methods is not utilized to get back to zero, Orum will eventually transfer funds from your collateral balance and we will ask you to refill your collateral balance.